Lesson 006 – Buybacks. The good, the bad and… your call

Hello, my Dear Readers, this is the Lesson #6 about Investing. And, as I promised in one of the previous lessons, I’m going to talk about stock repurchase programs (buybacks) in this lesson. Many beginners either undervalue (like me 7 years ago) or overvalue buybacks. Both are typically incorrect, and both will have to take bitter pills. I hope this article will reduce the amount of bitter failures in your investment career. Let’ start.

What is buyback

Buybacks is a program by which a company buys back its own shares from the shareholders, reducing the number of shares outstanding. The following example will illustrate this concept better.

The Good

Example: company A cannot expand its business anymore – the business is okay, but already reached its physical  limits. So, every year they report a growth on net income, but this is the growth mostly due to inflation and population increase. The management decides that every year they will buy back certain percentage of the shares outstanding. For me as a shareholder it means that now I own bigger and bigger share of the business: I still own the same amount of shares, but there are less shares outstanding.

limits. So, every year they report a growth on net income, but this is the growth mostly due to inflation and population increase. The management decides that every year they will buy back certain percentage of the shares outstanding. For me as a shareholder it means that now I own bigger and bigger share of the business: I still own the same amount of shares, but there are less shares outstanding.

Problem 10: Last year EPS was $1. This year 10% of the shares were bought back. Assuming that net income for this year will remain the same, what EPS should we expect? Assuming that the average P/E ratio for the company is 10, what was the average share price last year, and what average share price should we expect this year?

Sounds great. But can be better?

A management of the company typically has the following ways of using the profits:

- pay dividends;

- re-invest into the core business;

- save money for a rainy day;

- stock repurchase.

And the answer to the question above depends on the type of investor and a situation with the company. If we talk about an income investor, cash dividends is the preferred way (sure! Dividends is the main incentive for such an investor to buy shares in the first place). If a business is cyclical, the option #3 can make more sense if the management anticipates next downturn quite soon. If the company still has room for growth, and investing into its core business will be more beneficial for shareholders, the management should prefer option #2. And only if they ladled up all other possibilities, they should consider stock repurchase program.

What happens to the shares?

One of two: either they are physically destroyed (cancelled or retired) or they are stored at a company’s Treasury Stock account (we will talk about this account significantly later, when we will plunge into reading financial statements). In any case such shares cannot vote, there are no dividends on them and they do not count into the shares outstanding. It makes sense: a company cannot own itself!

Problem 11: Why would the management opt for keeping repurchased shares at Treasury Stock account rather than physically destroying them?

The Bad

Example: Company Z has 1,000,000 shares outstanding. Its net income for previous year was $1 mln. This year the management expects an income of $950,000. The management decided to buy back 5% of shares outstanding to mask this fact. As a matter of fact, EPS will remain $1, same as was last year.

management expects an income of $950,000. The management decided to buy back 5% of shares outstanding to mask this fact. As a matter of fact, EPS will remain $1, same as was last year.

We can see that the management wants to get shareholders tricked by earnings per share statistics. This is so called detrimental buybacks.

If you see that Net Profits declines, but due to buybacks EPS looks okay, steer clear of such companies! (unless, of course, you have a short-term speculative interest).

Shares Issuance

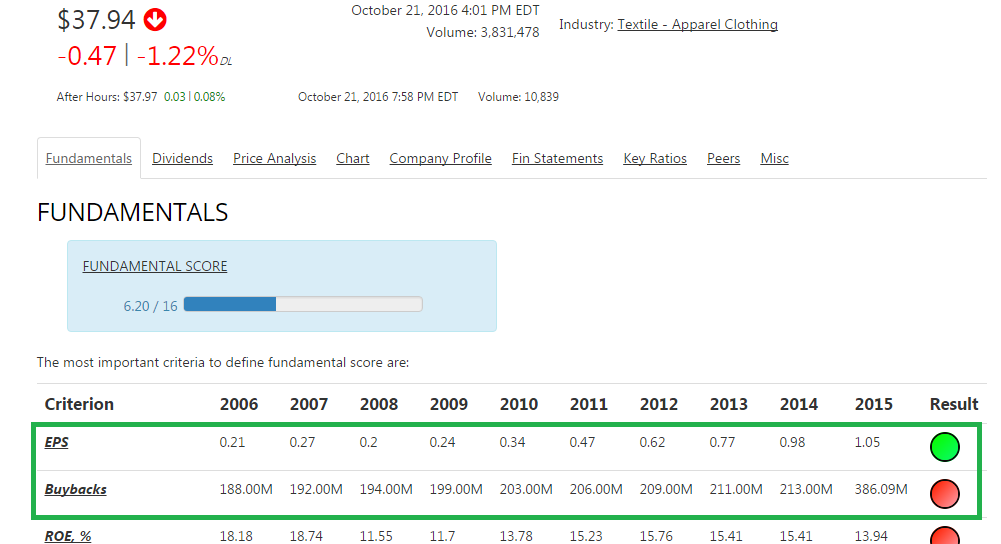

As opposed to stock repurchase you may see that some companies issue more shares. Of course, for you it would be rather bad to see that your ownership diluted as a result. Many investors consider such state of things unacceptable, and I totally understand them. But they potentially can miss extremely good investments by refraining from some of such companies. Please look at the partial screenshot from a company report at blackbeltinvestments.com below – it shows EPS and buyback stats:

As you can see, EPS grew 5 times and Shares Outstanding increased just 2 times during the same period. Provided that other company’s fundamentals are quite strong, I would put up with shares dilution. And yes, it is a real company… Under Armour Inc. Please, don’t get me wrong, I do not recommend this company in any wise. I’m just saying, that sometimes it makes sense to turn a blind eye on the fact that a company constantly issues more shares.

Thanks for reading and may the good buybacks be with you!

This is our next lesson regarding investments. It will be about the Golden Rules, or The Commandments Of Investor. Do not treat this list as just nice-to-know stuff: all these rules are written not in ink, but in sweat, blood and tears of many-many investors. Moreover, one of these rules is extremely important for us as for fundamental investors – I will stress it out later on in this lesson. Off we go!

This is our next lesson regarding investments. It will be about the Golden Rules, or The Commandments Of Investor. Do not treat this list as just nice-to-know stuff: all these rules are written not in ink, but in sweat, blood and tears of many-many investors. Moreover, one of these rules is extremely important for us as for fundamental investors – I will stress it out later on in this lesson. Off we go! mutual funds in this case: if the market goes down, your investment will shrink accordingly, and, if it happens, because of short time span, the market will highly unlikely recuperate by the time you need the money. Some may say: “Yeah, but I will invest into blue chips only!” That’s good, but the market risk affects them as well. Of course, they will probably be less impacted by any crisis and will recover very soon, but all this requires time (and since you need a car in 2 years, you may not want to wait, say, 4 years).

mutual funds in this case: if the market goes down, your investment will shrink accordingly, and, if it happens, because of short time span, the market will highly unlikely recuperate by the time you need the money. Some may say: “Yeah, but I will invest into blue chips only!” That’s good, but the market risk affects them as well. Of course, they will probably be less impacted by any crisis and will recover very soon, but all this requires time (and since you need a car in 2 years, you may not want to wait, say, 4 years).